Can a Spouse Rollover an Inherited IRA Into Their Own IRA?

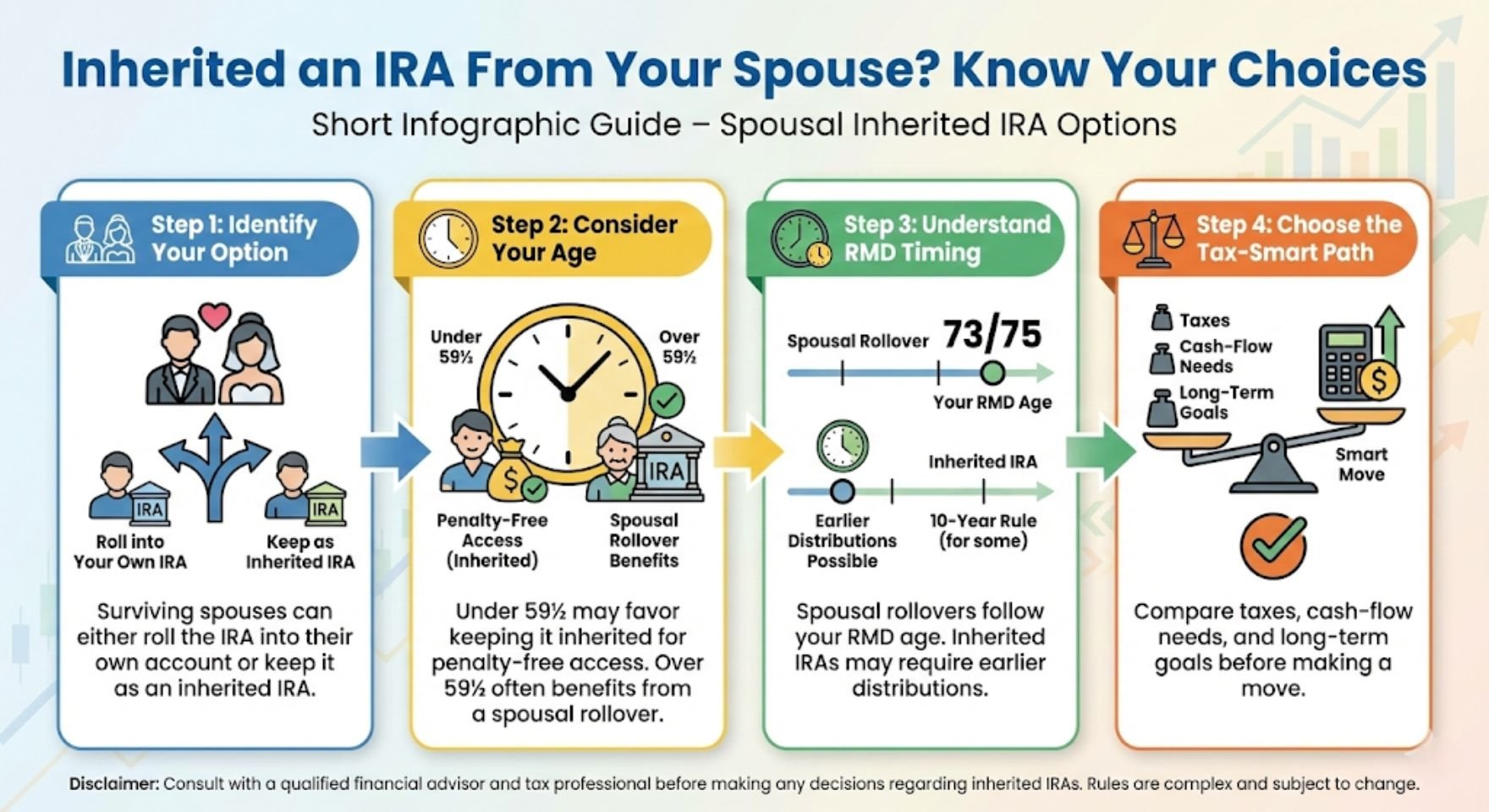

Yes, a surviving spouse is the one person who can roll an inherited IRA into their own IRA, but the rules, timing, and tax consequences depend on how the spouse chooses to treat the account. This flexibility can be extremely valuable, but the wrong choice can trigger unnecessary taxes or penalties. Understanding when a spousal rollover makes sense, and when it does not, is critical for long-term retirement planning.

Understanding the Unique Rights of a Surviving Spouse

When someone inherits an IRA, the IRS treats spouses very differently from non-spouse beneficiaries. A surviving spouse has options that no other beneficiary has, including the ability to fully absorb the inherited IRA into their own retirement account.

This special treatment recognizes that spouses often rely on shared retirement savings and may need more flexibility in how and when they access those funds.

The Spousal Rollover Option Explained

What a Spousal Rollover Is

A spousal rollover allows a surviving spouse to move assets from an inherited IRA into their own IRA or to re-designate the inherited account as their own. Once this happens, the IRA is treated exactly like any other IRA the spouse already owns.

From the IRS’s perspective, the inherited status disappears entirely.

How the Account Is Treated After the Rollover

After a spousal rollover, the account follows all normal IRA rules based on the surviving spouse’s age and tax profile. This includes:

Required minimum distributions beginning at the spouse’s required beginning age

Normal early-withdrawal rules before age 59½

The ability to name new beneficiaries

Eligibility for Roth conversions, if applicable

For many spouses, especially younger ones, this option provides the longest possible tax-deferred growth.

Required Minimum Distributions After a Spousal Rollover

When RMDs Begin

Once the inherited IRA is rolled into the spouse’s own IRA, required minimum distributions follow the spouse’s timeline, not the deceased spouse’s.

For most people, RMDs currently begin at age 73. This means a surviving spouse younger than that age can often delay withdrawals for years or even decades.

Why This Can Be Advantageous

If the deceased spouse was already taking RMDs, rolling the account into the surviving spouse’s IRA can stop those mandatory withdrawals until the surviving spouse reaches their own RMD age.

This delay allows:

Continued tax-deferred growth

Greater control over taxable income

More flexibility in retirement income planning

For younger surviving spouses, this is often the single biggest advantage of a spousal rollover.

Naming Beneficiaries After a Spousal Rollover

Once the IRA is treated as the surviving spouse’s own, they can name beneficiaries just like any other IRA owner. This includes:

Children

Grandchildren

Trusts

Charities

This reset can be important for estate planning, especially if the original beneficiary designations no longer align with the surviving spouse’s wishes.

When a Spousal Rollover May Not Be Ideal

While a spousal rollover is powerful, it is not always the best move.

Early Withdrawals and the 10 Percent Penalty

If the surviving spouse is under age 59½ and expects to need access to the money soon, rolling the IRA into their own name can create a problem.

Once the account is treated as the spouse’s own IRA, any distributions before age 59½ are generally subject to the 10 percent early-withdrawal penalty, unless an exception applies.

This penalty does not apply to inherited IRAs.

Cash Flow Needs Matter

Spouses who need near-term income to cover living expenses, medical costs, or debt often benefit from keeping the account as an inherited IRA rather than rolling it over immediately.

In these situations, flexibility today may matter more than tax deferral tomorrow.

Keeping the IRA as an Inherited IRA Instead

How Inherited IRA Rules Work for Spouses

Instead of doing a spousal rollover, a surviving spouse can leave the account titled as an inherited IRA. When handled correctly, this allows penalty-free withdrawals regardless of age.

The trade-off is that inherited IRA distribution rules apply.

RMD Timing for Spouse Beneficiaries

Spouse beneficiaries have more flexible RMD rules than non-spouse beneficiaries, but they are still different from owning the IRA outright.

Depending on the spouse’s age and the deceased spouse’s age, RMDs may begin sooner than they would under a spousal rollover.

This can increase taxable income earlier than expected.

Why Some Spouses Delay the Rollover

Many surviving spouses choose a hybrid approach. They keep the IRA as inherited while they are under 59½, then roll it into their own IRA later once early-withdrawal penalties are no longer an issue.

This strategy preserves flexibility while avoiding unnecessary penalties.

Comparing the Two Options Side by Side

Treating the IRA as Your Own

This option is often best when:

The surviving spouse is over age 59½

The spouse does not need immediate access to the funds

Delaying RMDs is a priority

Long-term tax planning and beneficiary control matter most

Keeping It as an Inherited IRA

This option is often better when:

The surviving spouse is under age 59½

The spouse needs access to the funds soon

Avoiding the 10 percent penalty is critical

Short-term cash flow outweighs long-term tax deferral

Non-Spouse Beneficiaries Do Not Have This Option

Only a surviving spouse can roll an inherited IRA into their own IRA. Children, siblings, and other beneficiaries cannot do this under any circumstances.

Non-spouse beneficiaries must keep the account titled as an inherited IRA and follow the applicable distribution rules, which typically involve:

The 10-year distribution rule for most beneficiaries

Life-expectancy distributions for certain eligible beneficiaries

Attempting to roll an inherited IRA into a personal IRA as a non-spouse beneficiary is a costly mistake that can result in immediate taxation of the entire account.

Common Spousal Rollover Mistakes to Avoid

Retitling the Account Too Soon

Rolling the account into your own IRA without considering near-term cash needs can trigger penalties that could have been avoided by waiting.

Missing Required Minimum Distributions

If the deceased spouse was already subject to RMDs, failing to take a required distribution in the year of death can create penalties, even if a rollover happens later.

Incorrect Account Titling

Inherited IRAs must be titled properly. Mistakes in account naming can cause the IRS to treat the transaction as a full distribution.

Ignoring Roth Conversion Opportunities

In some cases, partial Roth conversions before or after a rollover can reduce lifetime taxes. This requires careful planning but is often overlooked.

Tax Planning Considerations for Surviving Spouses

The decision to roll over an inherited IRA is rarely just about one rule. It interacts with:

Current and future tax brackets

Social Security timing

Medicare premium thresholds

Other retirement accounts

Estate planning goals

A choice that looks good on paper may create unintended tax consequences later.

Why Professional Guidance Is Often Worth It

Inherited IRA rules are technical, and penalties for mistakes are severe. Modeling both scenarios, treating the IRA as your own versus keeping it inherited, can reveal meaningful differences in lifetime taxes and cash flow.

For many surviving spouses, a short planning engagement with a tax or financial professional can save tens of thousands of dollars over time.

Final Thoughts on Spousal IRA Rollovers

A surviving spouse has a powerful and unique ability to roll an inherited IRA into their own IRA, but that power must be used carefully. The right choice depends on age, income needs, tax strategy, and long-term goals.

For some spouses, a spousal rollover is the best path to maximizing tax-deferred growth. For others, keeping the account inherited, at least temporarily, provides essential flexibility.

Understanding the rules before taking action ensures the inherited IRA continues to support financial security rather than creating avoidable tax problems.

Make the right move with your inherited IRA. Zag Consulting Group helps surviving spouses model rollover options, avoid costly penalties, and build a tax-smart retirement strategy with confidence.