Can You Roll Over a 529 Plan to a Roth IRA?

Yes, in many cases you can roll over a 529 plan to a Roth IRA, but only under the new SECURE 2.0 rules and only if several strict conditions are met. This option became available starting in 2024 and is designed to help families avoid penalties on unused education savings, not to create a new loophole for large Roth IRA funding.

Understanding how these rollovers work, who qualifies, and how much can be moved is essential before attempting a transfer.

The New SECURE 2.0 Rule Explained

What Changed in 2024

Before SECURE 2.0, unused 529 plan funds generally faced income tax and a 10 percent penalty on earnings if withdrawn for non-qualified purposes. Starting in 2024, federal law allows certain unused 529 plan assets to be rolled directly into a Roth IRA without triggering tax or penalties.

This change provides a safety valve for families who saved diligently for education but ended up with leftover funds because of scholarships, lower-than-expected costs, or changes in education plans.

Who the Roth IRA Is For

The Roth IRA receiving the rollover must belong to the same person who is the beneficiary of the 529 plan. The account owner of the 529 cannot roll funds into their own Roth IRA unless they are also the beneficiary.

This rule reinforces the intent of the law, which is to benefit the student or original beneficiary rather than providing a back-door retirement strategy for parents or grandparents.

Key Limits and Dollar Caps

Lifetime Rollover Maximum

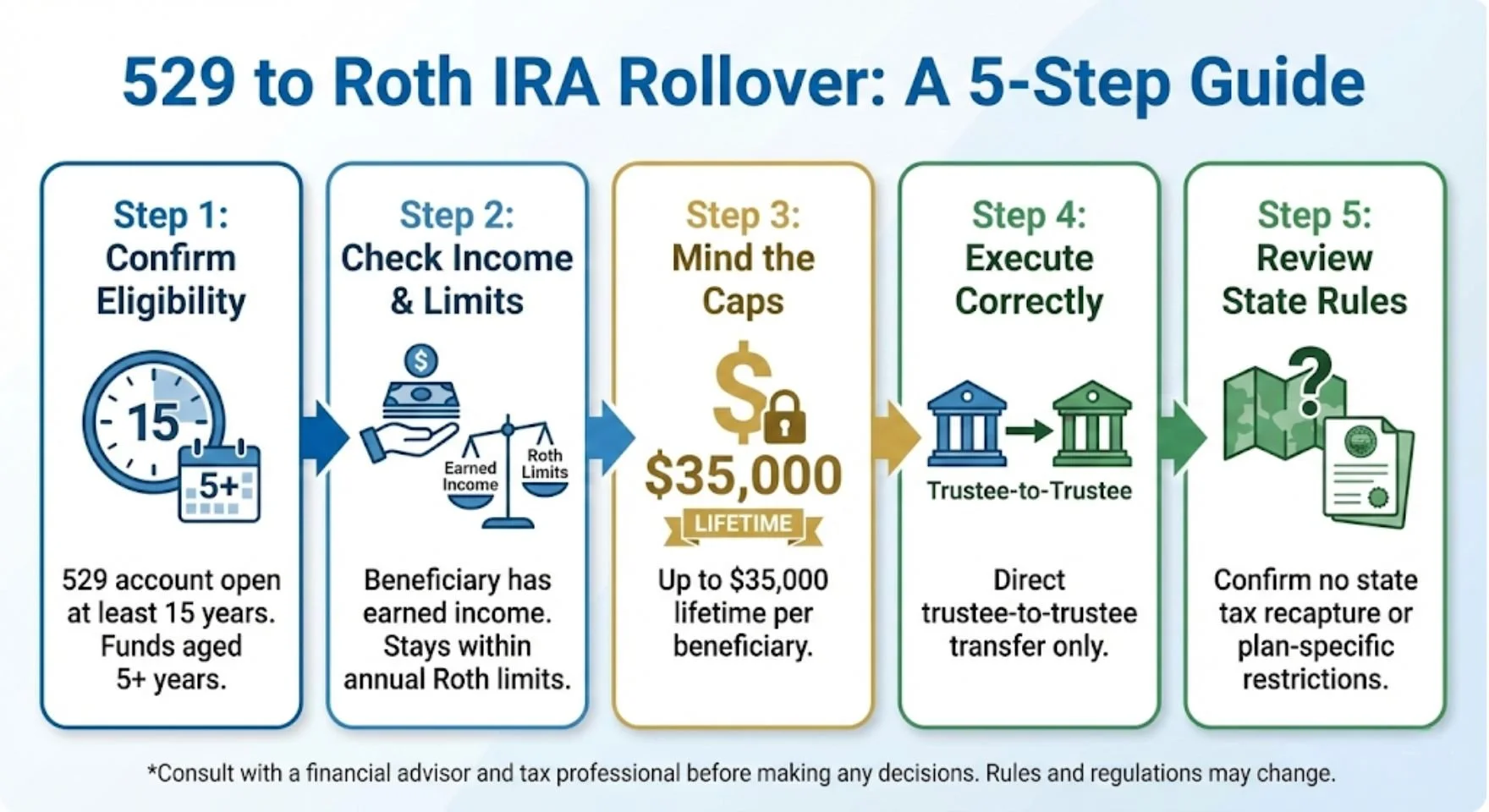

There is a lifetime cap of approximately 35,000 dollars per beneficiary that can be rolled from a 529 plan into a Roth IRA. This cap applies across all rollovers for that beneficiary, even if multiple 529 accounts exist.

Once the beneficiary reaches this lifetime maximum, no additional 529-to-Roth rollovers are permitted.

Annual Roth Contribution Limits Still Apply

Each year’s rollover amount is limited by the annual Roth IRA contribution cap in effect for that year. In recent years, this has generally been 7,000 dollars, or 8,000 dollars for individuals age 50 or older.

The rollover does not get its own separate limit. Any regular Roth IRA contributions made by the beneficiary during the year must be combined with the rollover amount and kept under the annual limit.

Earned Income Requirement

The beneficiary must have earned income at least equal to the amount being rolled over in that year. For example, if the beneficiary wants to roll over 6,000 dollars from a 529 plan, they must have at least 6,000 dollars of earned income for that year.

This rule mirrors standard Roth IRA contribution requirements and often becomes the main limiting factor for younger beneficiaries who are students or early in their careers.

Account Age and Holding Period Rules

The 15-Year Account Requirement

The 529 plan must have been open for at least 15 years for the current beneficiary before any rollover to a Roth IRA is allowed. This requirement applies to the account itself, not to when contributions were made.

Changing the beneficiary generally resets the 15-year clock, which can significantly delay eligibility. This makes beneficiary changes an important planning consideration for families thinking long term.

The 5-Year Contribution Lookback Rule

Even after the 15-year requirement is met, not all funds in the account may be eligible. Contributions and earnings associated with contributions made within the last five years are generally excluded from rollover eligibility.

This rule prevents last-minute contributions from being immediately converted into Roth IRA assets and reinforces the idea that the rollover is for genuinely unused education savings.

How the Rollover Must Be Done

Trustee-to-Trustee Transfers Only

The rollover must be completed as a direct trustee-to-trustee transfer from the 529 plan to the Roth IRA. The funds cannot pass through the beneficiary’s hands.

If the beneficiary takes a distribution from the 529 and then attempts to deposit it into a Roth IRA, the IRS will typically treat it as a non-qualified 529 withdrawal. That can result in income tax and a 10 percent penalty on the earnings portion.

Coordination With Roth Contributions

Because rollovers count toward the annual Roth contribution limit, careful coordination is required. If the beneficiary already made regular Roth IRA contributions earlier in the year, the rollover amount must be reduced accordingly.

Failure to track this correctly can lead to excess contributions, which trigger ongoing IRS penalties until corrected.

Roth Income Limits and Other Rules

Roth Income Limits Are Waived

One notable advantage of the 529-to-Roth rollover is that the usual Roth IRA income limits do not apply. Even high-income beneficiaries who would normally be ineligible for Roth contributions can still receive rollover funds from a 529 plan.

This feature is helpful for beneficiaries whose income rises quickly after graduation, but it does not override any of the other restrictions.

Other Roth Rules Still Apply

While income limits are waived, all other Roth IRA rules remain in force. Earned income is still required, annual contribution limits still apply, and the lifetime 35,000-dollar cap cannot be exceeded.

Additionally, the Roth IRA itself must be in the beneficiary’s name and properly established before the rollover occurs.

Why This Is Not a Roth Funding Strategy

Designed as a Safety Valve

Congress intentionally structured this rule with tight limitations. The goal was to reduce fear of overfunding education savings, not to create a new retirement planning shortcut.

The lifetime cap, earned income requirement, and long holding periods all work together to ensure that the rollover is used sparingly and only in appropriate situations.

Limited Use for High Balances

Families with large unused 529 balances will still face restrictions. Only a portion can ever be moved into a Roth IRA, and the process can take many years due to annual contribution limits.

For larger balances, other planning strategies may still be required, such as changing beneficiaries within the family or using funds for qualified education expenses.

State-Level Considerations

Possible State Tax Recapture

While federal tax law allows these rollovers, some states may have their own rules. Certain states that provided tax deductions or credits for 529 contributions may attempt to recapture those benefits if funds are rolled to a Roth IRA.

The treatment varies by state, and guidance is still evolving. This makes it important to review state-specific rules before initiating a rollover.

Plan-Specific Procedures

Not all 529 plans handle rollovers the same way. Some plans may require additional paperwork, specific timing, or confirmation of eligibility before processing a trustee-to-trustee transfer.

Checking with the specific 529 plan administrator is an essential step to avoid delays or errors.

Practical Planning Examples

Young Graduate With Leftover Funds

A college graduate with a small leftover 529 balance and part-time income may gradually roll funds into a Roth IRA over several years. This allows unused education savings to become long-term retirement assets without penalties.

Beneficiary With Rising Income

A beneficiary whose income increases quickly after graduation may benefit from the waived Roth income limits. Even if their earnings exceed standard Roth thresholds, they can still receive eligible rollover amounts.

Families Considering Beneficiary Changes

Because changing beneficiaries can reset the 15-year clock, families should weigh this carefully. In some cases, leaving the beneficiary unchanged and planning a future rollover may be more advantageous than reallocating the account.

Common Mistakes to Avoid

Attempting an Indirect Rollover

Taking a distribution and redepositing it yourself is one of the most common errors. This almost always results in taxes and penalties and defeats the purpose of the new rule.

Ignoring Earned Income Rules

Without sufficient earned income, the rollover cannot be completed, even if all other conditions are met. This often surprises families who assume student status alone is enough.

Exceeding Annual Limits

Combining regular Roth contributions with rollover amounts without tracking totals can easily lead to excess contributions and IRS penalties.

Final Thoughts

Rolling over a 529 plan to a Roth IRA is now possible under SECURE 2.0, but only within a narrow and carefully regulated framework. The 15-year account requirement, 5-year contribution rule, earned income requirement, annual limits, and lifetime cap all play critical roles in determining eligibility.

For families with leftover education savings, this option can be a powerful way to repurpose funds without tax or penalties. However, the complexity of the rules and potential state-level issues make professional guidance and careful planning essential before moving forward.

Turn leftover 529 funds into long-term tax-free growth. Zag Consulting Group helps you navigate the SECURE 2.0 rules, avoid costly mistakes, and execute your 529-to-Roth rollover correctly. Schedule a consultation and get clarity before you move a dollar.