How Many IRA Rollovers Per Year Are Allowed?

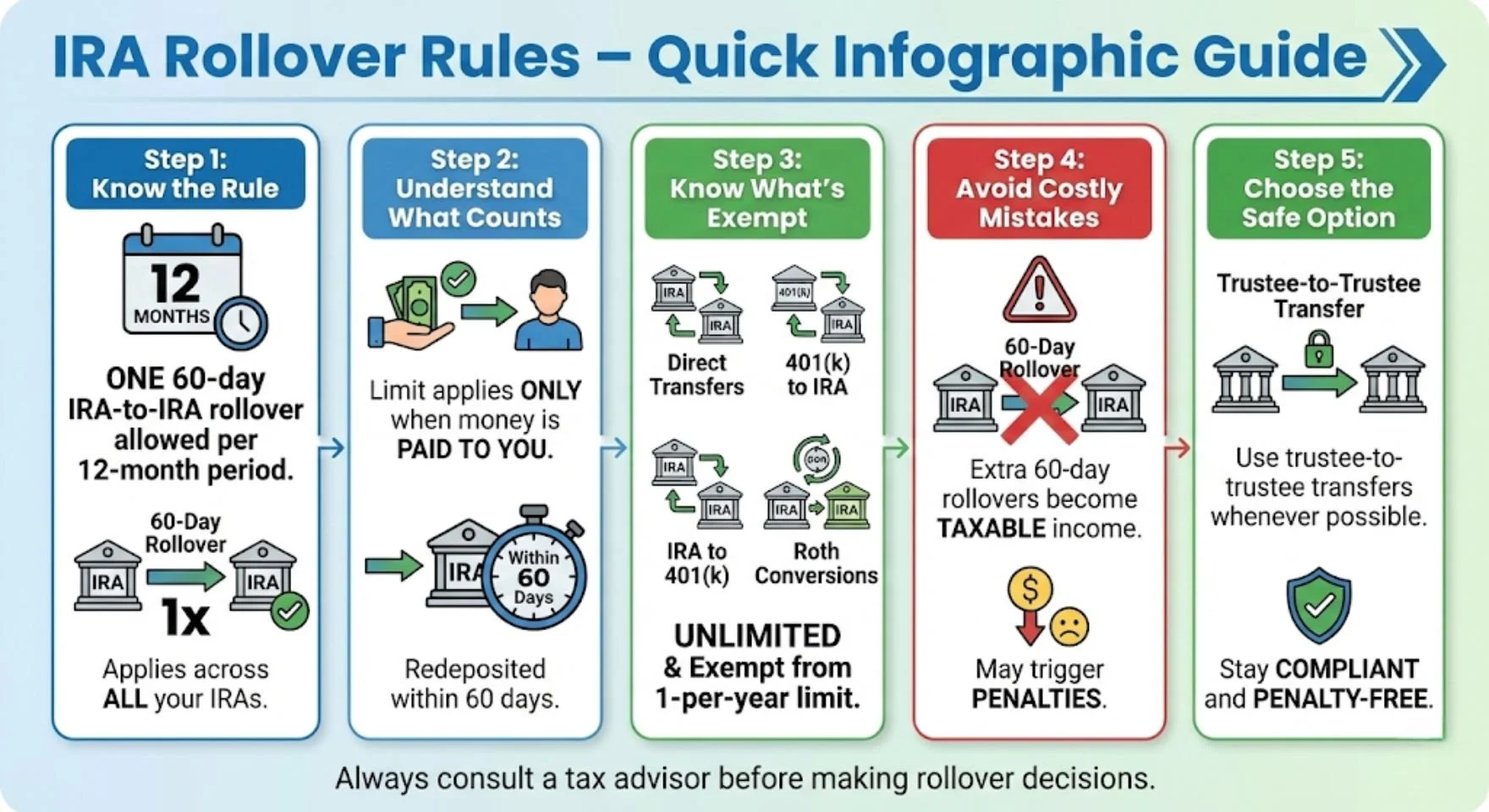

You are generally limited to one IRA-to-IRA rollover every 12 months, but that rule is far narrower than many people assume, and misunderstanding it can lead to unexpected taxes and penalties. The so-called one-per-year rule applies only to a specific type of rollover, while many common retirement account moves are completely exempt. Understanding how this rule actually works allows you to move retirement money safely, preserve tax advantages, and avoid costly mistakes.

What Is an IRA Rollover?

An IRA rollover occurs when retirement funds move from one account to another while maintaining their tax-advantaged status. Rollovers are commonly used when changing custodians, consolidating accounts, converting to a Roth IRA, or moving money from an employer plan into an IRA.

Not all rollovers are treated the same by the IRS. The key distinction is how the money moves and whether you personally take possession of the funds at any point.

Two Basic Ways IRA Money Can Move

There are two primary methods for moving IRA funds:

A 60-day rollover, where the money is paid to you first and you then redeposit it into an IRA within 60 days.

A direct transfer, also called a trustee-to-trustee transfer, where the money moves directly between custodians without ever touching your hands.

The one-per-year rule applies only to the first method.

The One-Per-Year Rule Explained

The one-per-year rule limits how often you can complete a 60-day IRA-to-IRA rollover. Under this rule, you are allowed only one such rollover in any 12-month period.

This is not based on the calendar year. Instead, it is a rolling 12-month window that begins on the date you receive the distribution from your IRA.

Why This Rule Exists

The IRS designed this rule to prevent people from using IRAs as short-term, tax-free loans. Without limits, someone could repeatedly withdraw funds, hold them temporarily, and redeposit them without tax consequences.

By restricting 60-day rollovers, the IRS ensures IRAs remain long-term retirement vehicles rather than flexible cash accounts.

The Rule Applies Across All Your IRAs

One of the most commonly misunderstood aspects of the rule is that it applies across all IRAs combined.

The one-per-year limit is not per account. It is per person.

That means if you have multiple IRAs, they are all grouped together for purposes of this rule, including:

Traditional IRAs

Roth IRAs

SEP IRAs

SIMPLE IRAs

Completing a single 60-day rollover from any one of these accounts starts the 12-month clock for all of them.

Example of How the Limit Works

If you take a distribution from a traditional IRA and roll it over within 60 days, you cannot do another 60-day rollover from a Roth IRA or SEP IRA until 12 months have passed from the date you received the first distribution.

This surprises many taxpayers who assume each IRA has its own rollover allowance.

What Does Not Count Toward the One-Per-Year Limit

The good news is that many of the most common and safest retirement account moves are not affected by the one-per-year rule at all.

Trustee-to-Trustee Transfers Are Unlimited

Direct transfers between IRA custodians are not considered rollovers. Because you never receive the money, these transactions are excluded from the limit.

You can complete an unlimited number of direct IRA transfers each year without triggering taxes or penalties.

This is why most financial professionals strongly recommend direct transfers whenever possible.

Plan-to-IRA Rollovers Are Exempt

Rollovers from employer plans into IRAs do not count toward the one-per-year rule. This includes:

401(k) to IRA rollovers

403(b) to IRA rollovers

457(b) to IRA rollovers

Pension lump sums rolled into an IRA

These transactions follow their own rules and are not restricted by the IRA rollover limit.

IRA-to-Plan Rollovers Are Also Exempt

Moving money from an IRA into an employer plan, such as rolling a traditional IRA into a 401(k), does not count toward the limit.

This can be useful for individuals who want to consolidate assets or clear pre-tax IRA balances before executing a Roth conversion strategy.

Roth Conversions Are Not Limited

Converting a traditional IRA to a Roth IRA is not subject to the one-per-year rule. Roth conversions can be done multiple times per year, although they may trigger income taxes depending on the amount converted.

This exemption is especially important for people using staged or partial Roth conversion strategies.

What Happens If You Break the Rule

Violating the one-per-year rule can be expensive.

If you complete more than one 60-day IRA rollover within a 12-month period, the extra rollover is treated as a taxable distribution.

Tax Consequences

The amount distributed becomes taxable income in the year you received it. If you are under age 59½, it may also be subject to a 10 percent early withdrawal penalty.

Excess Contribution Problems

If you attempt to redeposit the funds into an IRA after violating the rule, the IRS treats that deposit as an excess contribution.

Excess contributions are subject to a 6 percent penalty per year for as long as the excess remains in the account. Fixing the mistake often requires corrective withdrawals and amended tax filings.

Why Direct Transfers Are Usually the Best Option

Because of the risks involved with 60-day rollovers, most people are better served using direct trustee-to-trustee transfers.

Benefits of Direct Transfers

No risk of missing the 60-day deadline

No exposure to the one-per-year rule

No mandatory tax withholding

No chance of accidental taxable distributions

Direct transfers are cleaner, simpler, and far less error-prone.

Situations Where a 60-Day Rollover Might Be Used

In limited cases, a 60-day rollover may still be useful, such as when a custodian does not support direct transfers or when timing constraints require temporary access to funds.

However, these situations should be approached cautiously and usually with professional guidance.

Common IRA Rollover Mistakes to Avoid

Many costly IRA errors stem from misunderstanding how rollovers work.

Assuming the Rule Resets Each Calendar Year

The 12-month period is rolling, not January to December. Taking a distribution in October means the clock runs until the following October.

Thinking Each IRA Gets Its Own Rollover

The rule applies across all IRAs combined. One rollover affects them all.

Confusing Transfers With Rollovers

A direct transfer is not a rollover. This distinction is critical for staying within IRS limits.

Overlooking Mandatory Withholding

Some 60-day rollovers may involve tax withholding, which must be replaced out of pocket to complete a full rollover.

How to Safely Move IRA Money

If your goal is to move or consolidate retirement accounts while avoiding penalties, following a few best practices can make a significant difference.

Use Direct Transfers Whenever Possible

Request a trustee-to-trustee transfer directly from your IRA custodian. This keeps the transaction off your personal tax radar.

Track Dates Carefully

If you ever do a 60-day rollover, document the exact date you receive the funds and ensure the redeposit occurs well before the deadline.

Confirm Plan Acceptance Rules

Not all employer plans accept IRA rollovers, especially from Roth or SIMPLE IRAs. Always verify eligibility before initiating a move.

Seek Professional Guidance for Complex Moves

If you are coordinating multiple accounts, Roth conversions, or employer plan rollovers, professional oversight can prevent costly missteps.

Key Takeaways on the One-Per-Year IRA Rollover Rule

The one-per-year rule is much narrower than many people think, but the consequences of violating it are severe.

It applies only to 60-day IRA-to-IRA rollovers where you personally receive the funds.

It is limited to one rollover per 12-month period across all IRAs combined.

Direct trustee-to-trustee transfers are unlimited and not restricted.

Plan-to-IRA rollovers, IRA-to-plan rollovers, and Roth conversions are all exempt.

Because of these distinctions, most people should rely on direct transfers rather than 60-day rollovers whenever possible. Understanding how the rule truly works allows you to move retirement assets confidently, preserve tax advantages, and avoid unnecessary penalties while maintaining full control over your long-term financial strategy.

Talk to Zag Consulting Group before you move your retirement money. Our team helps you structure rollovers the right way, avoid IRS penalties, and make tax-smart decisions with confidence.