Can You Roll Over a SIMPLE IRA to a 401(k)?

Yes, you can roll over a SIMPLE IRA to a 401(k), but only if you follow very specific IRS timing and plan eligibility rules. The most important factor is whether you have satisfied the required two-year participation period in the SIMPLE IRA. If you attempt the rollover too early or into the wrong type of plan, the transfer can trigger income taxes and steep penalties. This guide explains exactly how SIMPLE IRA to 401(k) rollovers work, when they are allowed, and how to complete one correctly.

Understanding the SIMPLE IRA Rollover Rules

A SIMPLE IRA is a retirement plan commonly used by small employers because it is easy to administer and inexpensive to maintain. However, SIMPLE IRAs come with unique rollover restrictions that do not apply to traditional IRAs or 401(k) plans. These rules are enforced strictly by the IRS, and violating them can be costly.

The Core IRS Rule: The 2-Year Participation Period

The most critical rule governing SIMPLE IRA rollovers is the two-year rule. This rule is measured from the exact date you first participated in the SIMPLE IRA, not from when you made your first contribution and not from the beginning of a calendar year.

During the first two years of participation, your SIMPLE IRA funds are locked into the SIMPLE IRA system. You may only transfer or roll over those funds to another SIMPLE IRA during this period. Moving the money to a 401(k), a traditional IRA, or a Roth IRA before the two-year window closes is treated as an early distribution.

If you are under age 59½ and violate this rule, the IRS applies a 25 percent early withdrawal penalty, not the standard 10 percent penalty that applies to most other retirement accounts. In addition, the full distribution amount is included in your taxable income for the year.

Once the two-year period has fully elapsed, the restrictions ease significantly. At that point, your SIMPLE IRA funds can be rolled into a 401(k) or other eligible retirement plans without triggering taxes or penalties, as long as the rollover is done properly.

When a SIMPLE IRA Can Be Rolled Into a 401(k)

After you have met the two-year participation requirement, a rollover from a SIMPLE IRA to a 401(k) becomes possible. However, timing alone is not enough. The receiving 401(k) plan must also allow rollovers from SIMPLE IRAs.

Eligible 401(k) Plans

Not all 401(k) plans accept incoming rollovers from SIMPLE IRAs. While many do, especially larger or more flexible plans, acceptance is determined by the plan document itself. Some plans accept rollovers from traditional IRAs but exclude SIMPLE IRAs specifically.

Before initiating a rollover, you must confirm that the 401(k) plan explicitly permits rollovers from SIMPLE IRAs. This applies whether the 401(k) is sponsored by your current employer, a previous employer, or your own business.

If the plan does not accept SIMPLE IRA rollovers, attempting to force the transfer can result in the funds being rejected or mishandled, potentially causing a taxable event.

How a SIMPLE IRA to 401(k) Rollover Works

There are two main ways to move funds from a SIMPLE IRA to a 401(k) after the two-year period. One method is strongly preferred because it minimizes risk and administrative errors.

Direct Rollover: The Preferred Method

A direct rollover, also known as a trustee-to-trustee transfer, is the cleanest and safest way to move your SIMPLE IRA funds into a 401(k). In this process, the money never passes through your hands.

Your SIMPLE IRA custodian sends the funds directly to the 401(k) plan administrator or custodian. Because the funds are transferred directly between institutions, there is no tax withholding, no reporting of a distribution to you personally, and no risk of missing deadlines.

This method preserves tax deferral and avoids the possibility of accidental penalties. For most individuals, a direct rollover is the only approach that makes sense.

Indirect Rollover: Allowed but Risky

An indirect rollover is possible after the two-year rule has been satisfied, but it carries more risk. In this scenario, the SIMPLE IRA custodian sends the funds to you, usually by check. You then have 60 days to deposit the full amount into the 401(k) plan.

If you fail to complete the rollover within 60 days, the entire amount is treated as a taxable distribution. If you are under age 59½, penalties may apply as well.

Indirect rollovers also increase the risk of administrative mistakes, such as depositing the funds into an ineligible account or misreporting the transaction on your tax return. Because of these risks, indirect rollovers are generally discouraged unless there is no alternative.

Tax Treatment of a SIMPLE IRA to 401(k) Rollover

When done correctly and after the two-year participation period, rolling a SIMPLE IRA into a 401(k) is a non-taxable event. The funds retain their tax-deferred status, and no income tax is owed at the time of the transfer.

If the rollover is done incorrectly, the consequences can be severe. A premature rollover triggers ordinary income tax on the full amount. If you are under age 59½ and still within the first two years, the 25 percent penalty applies. Even after two years, early withdrawals that are not rolled over properly may still be subject to the standard 10 percent penalty.

Because of these stakes, verifying eligibility and using a direct rollover is essential.

Special Employer Conversion Situations

In some cases, a SIMPLE IRA rollover to a 401(k) occurs because an employer changes its retirement plan structure. These situations have additional nuances.

Employer Replaces a SIMPLE IRA With a 401(k)

When an employer terminates a SIMPLE IRA plan and replaces it with a 401(k), employees who have met the two-year participation requirement can typically roll their existing SIMPLE IRA balances into the new 401(k) plan without current tax consequences.

Employees who have not yet satisfied the two-year rule usually must keep their SIMPLE IRA balances in a SIMPLE IRA until the period expires. Even though the employer has moved on to a 401(k), the IRS rules still apply to each individual participant.

Midyear Replacement With a Safe Harbor 401(k)

Newer IRS rules allow certain employers to replace a SIMPLE IRA with a safe harbor 401(k) midyear. This is a more complex scenario that depends heavily on plan design, required notices, and contribution rules.

In these cases, whether employees can roll existing SIMPLE IRA balances into the new 401(k) still hinges on the two-year participation rule. Plan documents must be reviewed carefully to determine eligibility and timing.

Why People Roll a SIMPLE IRA Into a 401(k)

Many individuals choose to roll a SIMPLE IRA into a 401(k) once eligible because of the added flexibility and advantages a 401(k) can offer.

401(k) plans often have higher contribution limits, especially for employer contributions and catch-up contributions. They may also offer loan provisions, which SIMPLE IRAs do not allow. For business owners, consolidating retirement funds into a 401(k) can simplify long-term planning and reporting.

Additionally, some investors prefer the investment options or creditor protections available within a 401(k) compared to an IRA-based plan.

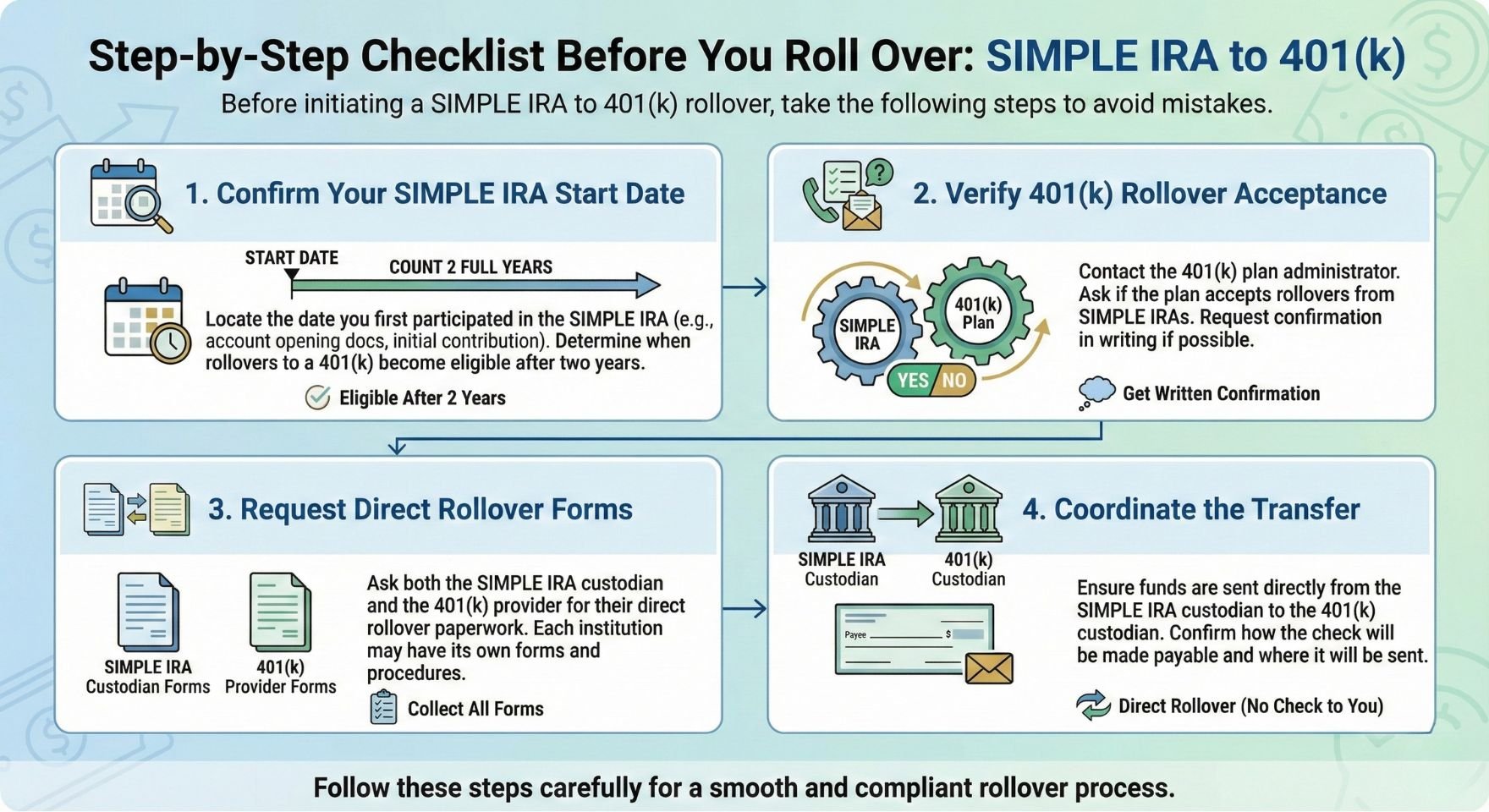

Step-by-Step Checklist Before You Roll Over

Before initiating a SIMPLE IRA to 401(k) rollover, take the following steps to avoid mistakes.

Confirm Your SIMPLE IRA Start Date

Locate the date you first participated in the SIMPLE IRA. This is usually shown on your account opening documents or initial contribution records. Count two full years from that date to determine when rollovers to a 401(k) become eligible.

Verify 401(k) Rollover Acceptance

Contact the 401(k) plan administrator and ask whether the plan accepts rollovers from SIMPLE IRAs. Request confirmation in writing if possible.

Request Direct Rollover Forms

Ask both the SIMPLE IRA custodian and the 401(k) provider for their direct rollover paperwork. Each institution may have its own forms and procedures.

Coordinate the Transfer

Ensure that the funds are sent directly from the SIMPLE IRA custodian to the 401(k) custodian. Confirm how the check will be made payable and where it will be sent.

Common Mistakes to Avoid

One of the most common errors is assuming that all IRAs follow the same rollover rules. SIMPLE IRAs are different, especially during the first two years. Another frequent mistake is relying on indirect rollovers and missing the 60-day deadline.

Failing to confirm that a 401(k) accepts SIMPLE IRA rollovers can also derail the process. These mistakes can be expensive and difficult to correct after the fact.

Final Thoughts on SIMPLE IRA to 401(k) Rollovers

Rolling a SIMPLE IRA into a 401(k) can be a smart move, but only if the IRS rules are followed precisely. The two-year participation requirement is non-negotiable, and the receiving 401(k) plan must explicitly allow the rollover.

For most people, a direct trustee-to-trustee rollover after the two-year window is the safest and most efficient approach. By confirming eligibility, coordinating with both custodians, and avoiding shortcuts, you can move your retirement savings without triggering unnecessary taxes or penalties and position yourself for greater flexibility going forward.

Talk to Zag Consulting Group before you move your SIMPLE IRA. We help you confirm the 2-year rule, verify 401(k) eligibility, and structure the rollover correctly so you avoid unnecessary taxes and penalties.